By Greg Hutto, CFP®, CFA®

As I have emphasized before, excessive concentration of company stock is a common source of financial problems for executives. Diversification can grow complex due to the number of different tools and structures, which can frankly introduce difficulty when deciding where to start. That’s why I put together the decision tree in this article to tie all the pieces together and quickly narrow diversification options to the few that make the most sense.

In previous editions of the Perceptive Executive Series, we have detailed various strategies to help an executive unwind concentrated stock positions. The use of exchange (swap) funds, prepaid variable forward sales, gifts to charitable remainder trusts, and collar strategies all have the potential to provide tax deferral or tax deductions, which can reduce single-stock risk, and can provide higher risk-adjusted returns over time.

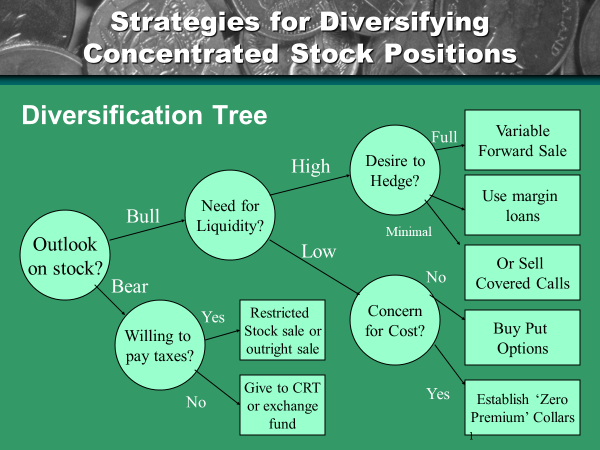

When you realize that it’s time to start walking down the “it’s-time-to-diversify” path, the following decision tree can help executives ask better questions when working with their advisors. The process of elimination can lead us to the most advantageous structure by focusing on five simple questions.

Let’s take a look at the decision tree, from your perspective, Mr. or Ms. Successful Executive, and examine each question.

Prepaid Forward Variable Sales

The first question focuses on outlook, because if you believe that a stock has significant upside potential, then your strategy needs to capitalize on additional potential gains from the current stock price. If a stock has performed well over the years, I’ve found it most effective to put strategies in place that can provide more runway for gains.

Let’s follow the decision tree and assume the answer to question #1 is “bullish.” Following the topmost route, let’s further assume that you need as much of the cash as possible right now and that your desire to hedge is strong. This pathway leads us to the use of a prepaid variable forward sale (PVFS).

This instrument can provide cash in the range of 85 to 90% of the value of the stock while providing 20-25% upside potential over the two- to three-year term of the forward sale agreement. A pretty good tradeoff, wouldn’t you say?

Margin Loans

In another scenario, let’s assume you’re bullish and that you need or want some cash from the transaction—but you don’t necessarily want to hedge most or all of the downside risk. In this case, the use of margin loans or pledged asset loans can fit the bill. A word of warning, though: This strategy has more potential negative consequences than positives. A client is exposed to leveraged downside risk when borrowing against securities, especially single stocks. The moral of the story: Be careful with margin or pledged asset loans!

Covered Call Options

The use of covered calls is often the go-to strategy when an executive wants to sell at a future higher price and doesn’t have a strong desire to protect against downside risk. Covered calls provide cash flow in the form of option premiums, but they don’t provide liquidity.

This pathway makes more sense if you are bullish on a stock over the long haul, but are not expecting short-term gains. Keep in mind that selling calls will obligate you to sell at the given strike price and contract date, so if the stock exceeds your expectations and appreciates above the strike price within the contract period, you can miss out on some of the gains.

Concern For Cost

Question #4 addresses situations with a bullish long-term outlook, but where short-term events can whack down the value of a stock temporarily. If you plan to hold a stock for the long haul and don’t need the cash right now—but believe you may want to sell in the intermediate future and have concerns about market volatility—you can follow one of two pathways.

If you’re looking at a fairly short window of time (say three months or less), then the cost to buy put options (even puts with strike prices that are close to the current stock price) may be insignificant. If the period is longer, you can set up a zero-cost collar strategy that will allow you to extend the time horizon and offset your costs by sacrificing some of the upside potential.

Strategies For Bearish Outlooks

Have you ever worked for a company where you would have rather been paid a higher salary, other benefits, or more perks, or pretty much anything other than RSUs or options? Unless you’ve been fortunate enough to be employed by incredible growth companies your entire career, you’ve likely looked at one or more of your option grants with the same “meh” anticipation of Granny’s Christmas fruitcake. A nice gesture—but you’d rather have something else. Let’s play out the scenarios when you’re bearish on your stock.

No one likes paying taxes, but it’s difficult to avoid paying taxes on an appreciated asset forever. If you just want out and you’re okay with the current price, then again, like with covered calls, sometimes simple is best. An outright sale at a permitted time can make sense if you just want out.

Finally, sometimes we want to have our cake and eat it too, by diversifying without incurring current or even future capital gains. Our article entitled “Everyone Can Win With a Charitable Remainder Trust (Except The IRS)” details the remarkable benefits of planned gifts like the powerful charitable remainder unitrust (CRUT). What’s the major downside to a CRUT? You are disinheriting your heirs with this strategy.

If you want to diversify your stock and still keep the proceeds available for your heirs when you’re gone, then gifting shares to a swap fund (aka an exchange fund) can make sense.

In our last article in the Perceptive Executive Series, we’re going to provide you with likely the most beneficial 8½” x 11” sheet of paper you’ve ever seen in your career. Stay tuned for the Executive Benefit Spreadsheet!

Give us a call this week at 817.503.0100 or email info@heritage-retirement.com to discuss how we can work together to build a financial strategy for you.

About Greg

Greg Hutto, president and CEO of Heritage Retirement Advisors, comes from a family of educators, so it’s no wonder he holds a bachelor’s degree in business from Texas A&M University, and a master’s degree in education from Tarleton State University. He spent years as a teacher and coach before entering financial services in 1996. After 14 years in the industry working for such powerhouses as UBS Paine Webber and Raymond James, Greg founded Hutto Retirement Advisors LLC in 2010, now Heritage Retirement Advisors. He holds both the Certified Financial Planner® (CFP®) and Chartered Financial Analyst (CFA®) designations. Additionally, he is the founder of Heritage Tax Advisors LLC. Greg and his wife, Angie, have three children. He likes to cycle, play golf, travel with his family. To learn more about Greg, connect with him on LinkedIn.