By Greg Hutto, CFP®, CFA®

Life isn’t fair. Unfortunately, that’s a life lesson learned early on for most of us. My mom used to give me great advice in response to this reality and would frequently say, “Just do the best you can with what you’ve got.” That’s all any of us can do, isn’t it?

The unfairness of life extends to the world of investments and investment structures. Have you ever had the suspicion that the very wealthy have access to investments that are not available to everyone? Well, this article will confirm your suspicions. You will likely be enthralled, and probably a little envious too. Let’s take a peek at how the 1% invests some of their money.

What Investment Structure Do You Dream About?

Before we talk specifics, let’s identify the characteristics of our ideal investment (or, better stated, our ideal investment structure), shall we? Our wish list might include the following:

- Tax-deferred accumulation

- Tax-free distributions

- Reallocations (buys and sells inside the account) not subject to capital gains taxes

- Strong asset protection

- A structure that can hold virtually any asset, both traditional and alternatives

- Gigantic contribution amounts permitted

The investment structure that you’re likely familiar with that best fits these characteristics is a Roth IRA. But the super-wealthy likely have never had a Roth IRA, and they probably never will; their income is above the threshold limits.

But don’t start a GoFundMe page for the mega-wealthy just yet. They do fine on their own without a Roth IRA, especially the ones who take advantage of this little-known gem in advanced planning.

What the super-wealthy desire is a structure just like a Roth IRA, only one that allows enormous contribution amounts. This structure would have the above-mentioned characteristics, including the last one listed in bold.

Life Insurance? Really?

Enter the best-kept secret in high finance, with quite the sales-y name: private placement life insurance. PPLI, as we’ll refer to it for the rest of this article, is, at its core, simply a variable universal life (VUL) policy that has been reconfigured for the needs of the super-wealthy.

You might be thinking, “Ah! I’ve heard of variable life insurance…,” and you’re probably none too impressed right now. If that’s been your attitude toward VUL, that they’re lousy products, then guess what? You’re right. Retail cash value policies usually are lousy products, because the fees and commissions embedded in the contract more than offset the great features that your buddy at the club keeps mentioning—namely the tax-deferred accumulation, and tax-free distributions.

The Fine Print

BUT…PPLI is different. It is a direct contract with a large insurance company and a wealthy couple or individual. It basically allows the mega-wealthy to invest in the asset classes they tend to prefer, such as private equity, hedge funds, and business interests, with a tax-protected wrapper around these investments. This tax-protected wrapper is especially important when assets have high returns but are tax-inefficient, like hedge funds and high-yielding bonds.

Let’s say a hedge fund has a gross (pre-tax) return of 10% over several years. That sounds pretty good, right? However, most hedge funds trade frequently and, as a result, almost all of the returns are short-term capital gains, which are taxed at ordinary income tax rates.

The top federal income tax bracket in 2020 is 37%, which means a fund with a pre-tax return of 10% that’s derived by short-term gains would only result in a 6.3% after-tax return for a top bracket payer. This same fund, if held in a PPLI contract, would provide the gross 10% return, minus the expenses of the contract, which we’ll detail later.

The Perks Of Special Funds

Which brings me to the next detail of PPLI—the investments in the contract require their own special funds. That 10%-returning fund I just mentioned can’t be offered in a PPLI contract if the exact same fund is available to retail investors. This results in a requirement for what is known as an IDF, an insurance-dedicated fund.

Often an IDF is formed as a “clone” of the retail version of a manager’s hedge fund, mutual fund, or separately managed account. So when a hedge fund manager gets a request to clone his or her fund as an IDF, then the manager will have two separate funds—one for the retail clientele and one IDF with a slightly different name (usually) that is, in essence, managed identically to the retail fund.

The carriers for PPLI have structured their offerings to look somewhat like a retail VUL contract, but with some important differences. Most major PPLI providers offer the same investment choices seen in a retail policy (all of the normal traditional asset classes like U.S. and international equity, small-, mid-, and large-cap funds, and bond funds).

The differences are in the pricing of the product and the willingness of carriers to include off-the-shelf investments. PPLI is almost exclusively offered in a fee-based (no commission) arrangement with very low mortality and expense charges and low-load (or no-load) funds within the contract. If a large investor is interested in having access to a fund or alternative asset that isn’t currently offered, then most carriers are willing to add this investment to the lineup.

And when structured correctly, PPLI can even pass assets outside of the family’s taxable estate upon the first generation’s passing. This simply means that the mega-wealthy can contribute huge sums of money into a contract and, when the patriarch and matriarch pass away, these assets won’t have estate taxes assessed on them. Why? Because they don’t own the assets; a life insurance trust owns the contract, not the insured. This is how assets can compound into truly gargantuan amounts over a 30-, 40-, or 50-year period—because they’re compounding without income taxation on the capital gains, dividends, interest, or even future estate taxes.

If You’re Saying, “Sign Me Up, Please!” Just Hold Your Horses

All of this sounds too good to be true, right? There’s a little catch to all this—it’s a life insurance policy. And as such, a person needs to have a desire for and willingness to obtain life insurance on their life, or preferably both spouses if we’re talking about a couple.

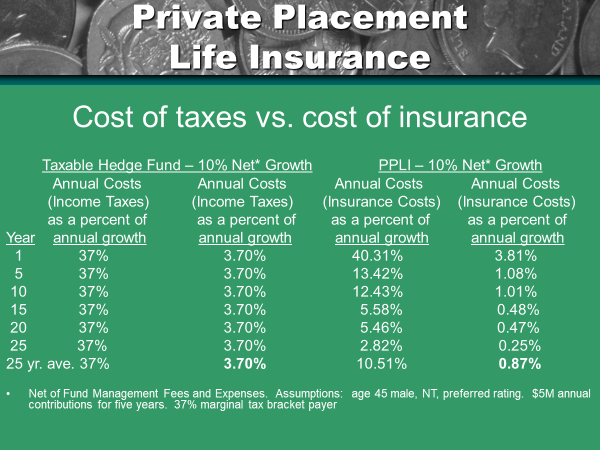

The determining factor as to whether it would behoove an investor to allocate some of their wealth to PPLI often comes down to this: the cost of insurance vs. the cost of taxes. The chart below can help describe this dynamic:

The takeaway on this concept is this: income taxes will always reduce the gross returns of an investment by a fixed percentage (if tax rates are assumed to be constant in the future), but the COI will go down significantly over time as a percentage of the contract value because of the growth of funds inside of the contract.

Obviously, the younger and healthier the insured is, the better, because the COI (cost of insurance) is lower, resulting in less “drag” and higher net returns. Nonetheless, this can still be a valid structure to consider if the insured is in their 60s, especially if both partners in a couple apply for coverage.

Specific rules govern how much life insurance must be purchased compared to the amount of premium invested. The “cash corridor” test and the calculations behind it are beyond the scope of this article, but again, don’t pity the rich—they’re not having to buy much life insurance in order to receive these tremendous benefits.

The amount of tax-free withdrawals that are available (if needed) for this hypothetical 45-year-old in 20 years, when 10% gross returns are assumed, can be staggering. I’m not going to provide a table of what that can look like—you may already be resentful from what you’ve read so far!

Okay, Now Can I Sign Up?

Think you might be a candidate for PPLI? The net worth at which PPLI usually starts to make sense is around the $20M level. But this amount could be much less, especially if income won’t be needed. When income isn’t desired, then a PPVA (private placement variable annuity) contract owned by an irrevocable trust may be a better choice, because the investor doesn’t have to pay for life insurance with PPVA.

Please contact me at info@heritage-retirement.com or 817.503.0100 if you would like more information about private placement life insurance. Next up in the Perceptive Executive Series: “You’re Too Successful To Pay For Your Own Life Insurance.”

About Greg

Greg Hutto, president and CEO of Heritage Retirement Advisors, comes from a family of educators, so it’s no wonder he holds a bachelor’s degree in business from Texas A&M University, and a master’s degree in education from Tarleton State University. He spent years as a teacher and coach before entering financial services in 1996. After 14 years in the industry working for such powerhouses as UBS Paine Webber and Raymond James, Greg founded Hutto Retirement Advisors LLC in 2010, now Heritage Retirement Advisors. He holds both the Certified Financial Planner® (CFP®) and Chartered Financial Analyst (CFA®) designations. Additionally, he is the founder of Heritage Tax Advisors LLC. Greg and his wife, Angie, have three children. He likes to cycle, play golf, travel with his family. To learn more about Greg, connect with him on LinkedIn.